Get monthly updates on FP&A best-practices and more.

Small businesses are under a tremendous amount of strain right now. Lost revenue, decreased productivity, supply shortages, staffing issues...the list goes on...

While there will always be trying times over the lifetime of a small business, it's hard not to get worried when more cash is flowing out of your business than in. We get it. Clockwork is a small business, and we come from small business families. Our communities are literally built around small businesses so we want to make sure they have the tools and resources to help them make it through whatever the next economic obstacle is.

If you’re a small business owner or advisor, and you’re feeling the financial impact of the slowing economy or the continued fallout of COVID-19, we're here to help.

Things you should be doing right now to manage your cash flow

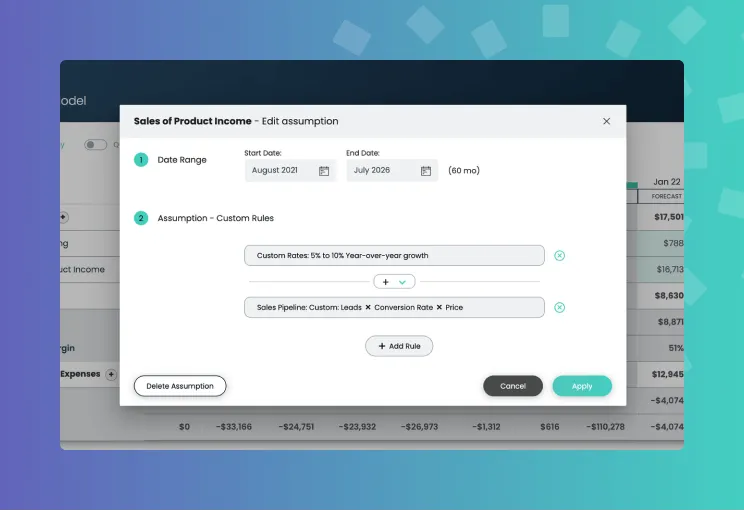

1. Understand your financial position

One of the first things you should do is update (or build) your weekly cash flow forecast. Make sure it’s accurate, uses the most up-to-date information available, and incorporates a couple of “what if” scenarios based on possible outcomes.

There is quite a bit of uncertainty right now, but getting a handle on your current cash situation, and how it could change week-to-week, is a critical starting point to formulating an action plan. You’ll want to look for future periods when cash will be dangerously low, or run out entirely, and figure out how much money you’ll need to keep the lights on.

Your accountant should be able to help, but if you have any questions you can also get in touch with our team. We live and breathe cash flow forecasts, and we’ll get you squared away.

2. Know your cash flow options

There are many strategies for optimizing cash flow, like accelerating collections, or delaying bill payments, but when things are this extreme, you may need some outside financing to bridge the gap. As long as your business wasn’t already tanking before the pandemic hit, local banks or investors should be viable sources of capital to keep you afloat. However, you’ll need to be careful to ensure you don’t structure a deal that will hurt you in the long run.

Trust your numbers. Don’t take on more funding than you need, or more than you can ultimately pay back. Debt often comes with covenants, and the more money you take, the more restrictions you’ll need to deal with. If you’re getting a loan, review the terms carefully to ensure you won’t break any covenants in a prolonged period of distress, and also that you won’t be restricted from operating normally when things recover.

Additionally, if you’re seeking an equity investment, be wary of any investors who ask for too much ownership or operational control in your company. Economic distress often leads to predatory investment behavior, and the last thing you want to do is give away your company for a quick buck.

3. Don't go it alone

For those businesses hit particularly hard, you have options. Economic relief packages are still available and while some SBA loans might be capped for the time being, government assistance is still available. Explore both federal and local programs for small businesses.

Here is a place to start if you're seeking out financial assistance.

4. Stay focused

Things are always changing and we still aren't out of the woods. Your cash flow forecast needs to be updated constantly so you’re not caught off guard and you can quickly adjust your plans with the latest information. Even if you get some funding, you still need to keep a close eye on your financials to make sure you don’t trigger any covenants or waste the capital when you need it most.

It’s ok to check the news a little more than normal, but your primary focus needs to be on the things you can control, so you’re not missing out on critical business information. Cloud-based tools like Clockwork have made this easier than ever, by providing real-time financial projections and insights, but they won’t do you any good if you’re not using them.

These are crazy times, but we’ll all get through it together. Our team is always here to help with any of your forecasting and cash flow management questions.

Conclusion

As a small business owner it's hard not to worry when more cash is flowing out than in. We want to make sure you have the resources to get through it.

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.webp)

.avif)

.png)

.avif)

.avif)

.avif)