Get monthly updates on FP&A best-practices and more.

In the evolving landscape of accounting, the most forward-thinking firms recognize the necessity of offering advisory services. This strategic expansion not only opens avenues for increased revenue through added value but also meets the rising client demand for such services.

By establishing an efficient pricing strategy, deepening client relationships, and staying competitive, firms can navigate the changing dynamics of the accounting industry with success.

7 Common Challenges (and Solutions) to Implementing Advisory

The transition to offering advisory services isn't just a shift in services; it's a transformation in approach and mindset. The real challenge lies not in deciding whether to offer advisory services but in how to effectively implement and scale these offerings. Below, we explore the seven common challenges accountants face in this journey and offer solutions to navigate these obstacles.

1. Acquiring Advisory Clients

Clients in search of advisory services are looking for more than number-crunching; they seek a partner who can provide strategic insights, help navigate financial complexities, and offer proactive advice to drive their business forward. They value a blend of technical accounting skills, strategic foresight, and a deep understanding of their business model and industry challenges. To these clients, an advisor is not just a service provider but a pivotal part of their decision-making process.

Solution

The first step is for your firm to internally prioritize advisory services as a core business offering. This means aligning team goals, resources, and training to support this strategic shift. Leadership must communicate the importance of this transition, ensuring that all team members are engaged and understand their roles in promoting and delivering advisory services.

Second, conduct a thorough review of your current client roster to identify businesses that may benefit from more strategic financial guidance. Look for clients who are in a growth phase, facing industry changes, or previously expressed interest in strategic planning or financial analysis.

We recommend checking out this article by Accounting Today on how to create your business plan.

2. Establishing a Pricing Strategy

Creating a pricing strategy for advisory services is one of the most nuanced challenges accounting firms face as they expand their offerings. Unlike traditional accounting services, which often follow a more standardized pricing model, advisory services demand a tailored approach that reflects the unique value they provide to each client. So, how do you develop an effective pricing model while still valuing the skillset that you bring to the table?

Solution

Start with a thorough analysis of the market. This includes researching what competitors are charging for similar advisory services and understanding the broader economic landscape of the industries you serve. However, it's crucial to go beyond just numbers; try to understand the value proposition and service delivery models of your competitors as well.

Additionally, the cornerstone of your pricing strategy should be the value your advisory services bring to your clients. This requires a deep understanding of your clients' business models, challenges, and the impact your services have on their growth and efficiency.

There are a few ways that we recommend developing your pricing structure:

- Value-Based Pricing: Consider adopting a value-based pricing model, which sets prices based on the perceived value to the customer rather than the cost to deliver the service. This approach aligns your interests with your clients' success and encourages your team to focus on delivering high-quality, impactful advice.

- Tiered Pricing Structures: Offering tiered pricing options can cater to a broader range of clients by providing different levels of service at different price points. Each tier should clearly define the services offered, allowing clients to choose a level that matches their needs and budget.

- Customizable Packages: Given the bespoke nature of advisory services, customizable packages can be highly effective. They allow clients to tailor services to their specific needs, demonstrating flexibility and client-centricity in your approach.

Check out this podcast episode of The Real Slim Fady Show with Clockwork founder, Fady Hawatmeh and accountant business coach, Reza Hooda. They do a deep dive into pricing strategy and how it impacts your business.

3. Evolving Skill Sets

The transition of an accounting firm into the advisory space demands more than a change in services offered; it requires a profound transformation in the skill sets of its professionals. Advisory services encompass a wide range of disciplines including financial forecasting, scenario planning, data analytics, and beyond. This evolution in skill sets enables accountants to provide value-driven advice and strategic insights that help clients navigate complex business landscapes and make informed decisions.

Solution

Identifying gaps in your team's skill set and seeking out targeted training programs and certifications is the first step. This can include specialized courses in financial modeling, business strategy, data analytics, and leadership.

Platforms like CPA Practice Advisor offer a wealth of resources tailored to the evolving needs of accountants. These platforms provide webinars, online classes, and articles that cover a wide range of topics relevant to advisory services. Some of their offerings include Continous Professional Education (CPE) credits, which can help maintain your team’s certifications.

4. Juggling Time

The integration of advisory services into a traditional accounting firm presents a complex challenge of time management. As firms strive to offer value-added advisory services alongside their core accounting functions, they encounter the need for a strategic approach to balance these demands effectively, especially during peak seasons when the workload intensifies.

Solution

Effective time management starts with prioritizing tasks based on urgency and importance. Use tools like Eisenhower's Matrix to categorize tasks and allocate your time accordingly. Planning your workload can help in balancing urgent compliance tasks with the strategic nature of advisory services. You can also use time blocking to allocate specific periods to advisory work, even during peak times. This dedicated time ensures that advisory services are not sidelined and that clients receiving these services feel valued and attended to.

Automation tools can significantly reduce the time spent on routine accounting tasks. Invest in software that automates repetitive tasks such as data entry and report generation. This not only speeds up traditional accounting work but also reduces errors, freeing up time for advisory services. We’ll talk more about that below!

Discover more time-saving tips in this article by Certified Tax Coach.

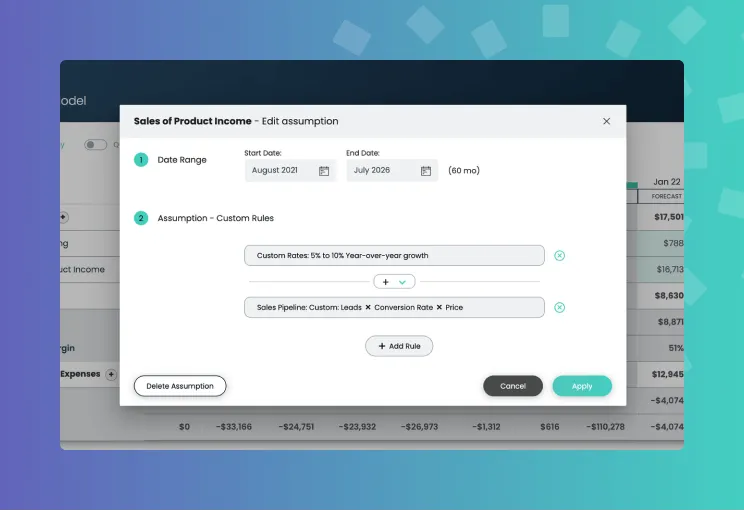

5. Integrating New Technology

The integration of new technology, and especially AI nowadays, is pivotal for accounting firms venturing into or expanding their advisory services. Technology can automate routine tasks, provide advanced analytics, facilitate deeper insights, and save a whole lot of time. However, the transition to new technology often comes with its set of challenges, such as adoption and training. Because of this, it’s important to evaluate which platforms will integrate most seamlessly with your firm.

Solution

Since there are a multitude of AI-powered accounting software on the market, we recommend trying a few that are truly advisory-focused and offer personalized support. This will help ease your transition into using new technology. After the technology is integrated, continuously monitor its usage, effectiveness, and impact on advisory services. Be open to making adjustments, whether in processes, additional training, or even reconsidering the tool if it does not meet expectations.

Check out how a forward-thinking firm, CloudCPA, found the best tech stack for them.

6. Standing Out

In the competitive landscape of advisory services, simply adding these offerings to your firm's portfolio is not enough to capture the attention of potential clients. To truly stand out, your firm must articulate a clear value proposition and communicate what makes your advisory services unique. This differentiation is crucial for attracting clients who are not just looking for any advisor but are seeking a partner that aligns with their specific needs and goals.

Solution

First, identify your firm’s Unique Selling Points (USPs). Determine what sets your advisory services apart from the competition. This could be your specialized expertise in a certain niche, your approach to financial planning and analysis, or your innovative use of technology. Your USPs should address specific client needs and highlight the benefits clients receive by working with you.

Check out these examples of accountants who specialize in specific industries:

Second, focus on the benefits your advisory services bring to clients, such as improved financial performance, risk mitigation, or strategic growth opportunities. Clients are more interested in how your services can help them achieve their goals than in the technical details of the services themselves.

Read this article by Gusto about the top niches of the most successful accounting firms.

7. Deepening Client Relationships

Deepening client relationships is a crucial step beyond client retention. It involves transforming existing relationships into more meaningful partnerships where the accountant is not just a service provider but an indispensable advisor. This transformation is essential for uncovering new business opportunities, providing more comprehensive services, and ultimately contributing to both the client's and the firm's success.

Solution

Advisors truly need to be proactive and stay in touch with their clients while being open to feedback. Schedule regular check-ins with clients, not just during the fiscal year-end or tax season. These check-ins can be used to discuss the client's current business environment, the challenges they are facing, and strategies for the future. It shows that you are invested in their success beyond the standard scope of work.

Additionally, it’s important to regularly solicit feedback on your services and use this input to improve and adapt your offerings. This not only helps in fine-tuning your services but also shows clients that their opinions are valued and taken seriously.

Discover more tips on how to deepen client engagement in this article by Accounting Today.

Looking to Stay Ahead of the Competition?

If you’re searching for an AI-powered accounting software that has seamless integration and dedicated support, Clockwork is at the forefront for firms that want to expand their advisory.

Time to get out of “spreadsheet hell” and start transforming data into actionable advice. By simplifying time-consuming processes such as cash flow forecasting and scenario planning, Clockwork enables firms to set up and receive a full dashboard of custom insights within just 3-5 minutes.

Start your 14-day free trial (no credit card required!) or speak to our team about how Clockwork can help you become an indispensable advisor to your clients.

Conclusion

Discover the solutions to seven common challenges for accounting firms looking to expand their advisory services.

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.webp)

.avif)

.png)

.avif)

.avif)

.avif)