Get monthly updates on FP&A best-practices and more.

Given the current economic climate, there’s been a heightened focus on cash flow management and forecasting. However, before you jump at the cheapest solution, or plug your numbers into a cookie-cutter template, it’s important to consider whether you’re actually choosing the right tool for the job.

Make sure you ask the right questions and use a forecasting model that’ll give you accurate insights and cut down on your overall workload. Otherwise, you’ll end up wasting your time and putting your trust in incorrect numbers, which will only cause more problems in the long run.

Cash flow forecasting: 3 big pitfalls to avoid

Mistake #1: Only looking at the P&L

Unless you immediately collect all revenues as cash, pay expenses exactly when they are recognized, never use credit cards or debt, and don’t invest in equipment or other fixed assets, Net Income alone will not reflect your cash flow realities. P&L forecasts are still important for business planning, but they only tell part of the story. Even a “cash basis” P&L forecast will fall short on reflecting all of the cash moving in and out of your business. Forecasting your P&L is only the starting point of a good cash flow projection.

Mistake #2: Hyper-focus on receivables and payables

Another common mistake is focusing too much on existing Accounts Receivable and Payable in the cash flow forecast. Existing invoices and bills play an important role in cash flow, but your A/R and A/P only tell a fraction of the story. What about all of your future business activities that aren’t yet booked as receivables and payables? Not to mention the other balance sheet movements from credit cards, debt, dividends, etc.. Many forecasting solutions hyper-focus on receivables and payables, but if you ignore all the other factors impacting your bank account, you’ll end up with an inaccurate (i.e. useless) forecast.

Mistake #3: Driver-based forecasting

Driver-based forecasting and other indirect methods can seem like “quick and dirty” ways to build a working projection, but when you only look at summary level data, or drive your projections based on generalized ratios and metrics, you’ll end up with a forecast that’s only loosely based on reality, and useless for any real-time tactical planning. Driver-based forecasting can give you a rough idea of the levers to pull in your business and how they impact your finances in theory, but if you need an accurate weekly cash flow projection, the margin for error using drivers and other indirect methods is just too large - you’ll never even get close to the real numbers.

What does it take to build a reliable cash flow forecast?

1. Start with the P&L

Map out your business plan and operating activities for at least the next 6-12 months. The P&L is only one portion of the cash flow forecasting equation, but you’ll want to make it as accurate as possible, so be realistic about your sales projections, make sure that your fixed expenses are accurately planned out, and properly tie your variable expenses to the level of business activity you’re expecting in each period. In this step, don’t worry about the cash flow timing associated with the P&L forecast - that comes next.

(Note: before incorporating forecasted P&L activities into your cash flow projections, make sure to add-back or remove non-cash expenses like depreciation, as these expenses will not affect your cash position)

2. Translate the P&L into cash inflows and outflows

Each week, there are forecasted revenues and expenses on the P&L which need to be translated into cash flow. A portion of your revenues may be collected right away, but the rest will be collected in future weeks, depending on your collection terms, the reliability of your customers, and many other factors. The same concept applies to expenses and bills. Cost of Goods Sold are typically booked on the P&L when a sale is made, but if you’re selling physical goods, you likely paid for that inventory long ago. And in other cases you may have payment terms with vendors that allow you to pay for COGS or other expenses at a later date, or to pay by credit card. If your cash flow model isn't properly reflecting the true cash movements associated with these P&L activities, you'll never come close to having an accurate weekly projection.

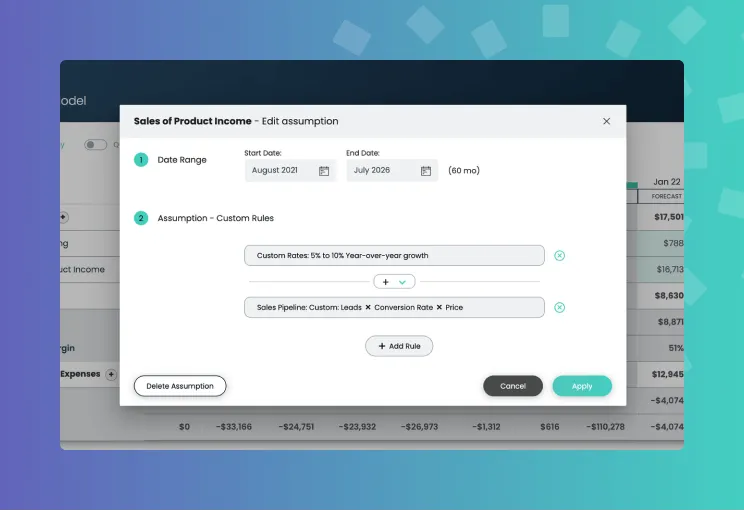

Clockwork uses AI to learn this behavior from your historical transaction activity and apply it to your forecast, but you can also make these assumptions on your own. The key is to understand that forecasted revenue does not automatically mean “cash in,” and expenses don’t necessarily mean “cash out” in the same period. Over-generalizing will throw your projections way off, so knowing the timing around all this activity (and actually incorporating it into your model) is critical to getting an accurate cash flow forecast.

3. Layer on the existing receivables and payables

Most likely, you have reasonably-certain cash inflows and outflows sitting around in the form of existing invoices and bills, but simply looking at the open balances and due dates on your receivables and payables is not enough. There may be certain customers who never pay on time, or have been severely impacted by economic conditions. You may also have opportunities to pay your bills late. It’s important to look at each invoice and bill, be realistic about how much will be collected/paid in each case, and on which dates you expect that to happen. Once you’ve made your best assumptions, apply the invoices as cash inflows, and bills as cash outflows on their respective dates in your model, and don’t forget to update these assumptions as new information becomes available.

4. But wait...there’s more!

Will you be taking on short term funding? Purchasing any assets or equipment? Pushing out dividends or paying down a loan? There are a number of cash-related activities that don’t show up on the P&L, or in your receivables and payables. Don’t forget that these will also impact your cash flows, and make sure to incorporate the one-off inflows and outflows in your forecasts.

5. Last but not least, the “what ifs”

Your base case is your working assumption about what’s going to happen, but in uncertain times, things could quickly change. Now more than ever, you’ve got to build out a couple of scenarios beyond your main forecast. You should at least have a best- and worst-case scenario built out, so you’re prepared for wild swings. It also helps to build scenarios for various decisions you’re considering, from reducing headcount, to taking on funding, and even shutting down temporarily. We can’t stress this one enough: when you're planning around unknown factors or major decisions, scenarios are the best way to prepare for the potential outcomes.

Final Thoughts: Time is Money

We talked about the importance of timing in your cash flow forecast, but you should also consider the time-cost of building the forecast itself. An accurate cash flow forecast is a lot of work, and when you also need to focus on running your business, can you really afford to spend hours in a spreadsheet fumbling around with the numbers by hand? In all likelihood, you’ll need a tool to automate the bulk of your forecasting so you can be present in your business. And when it comes to efficiency, Clockwork is second-to-none.

When you connect your company to Clockwork, we’ll automatically build out an AI-powered P&L and cash flow forecast that talk to each other in real-time, and learn from the transaction level data from your accounting system with each hourly update. You can dial in the forecasting rules on the P&L, override the balance sheet and receivable/payable assumptions, and easily build scenarios with just a few clicks, but the back end AI will handle the rest, to make sure everything is as accurate and real-time as possible. You've got a business to run, after all.

Conclusion

Make sure you ask the right questions and use a cash flow forecasting model that’ll give you accurate insights and cut down on your overall workload.

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.webp)

.avif)

.png)

.avif)

.avif)

.avif)